Are you thinking about selling your small business? If so, now is the time to start setting yourself up for a clean, successful exit. Without financial advice for small businesses, you might not get the outcome you want. However, with it, you can attend to the right details long before you initiate the sale process. That puts you in a position to avoid problems, get a better deal, and have a stress-free transaction. With the following expert tips, you can position yourself to benefit more from your future sale.

Are you looking for a financial services team to help you prepare for selling your small business? Contact Financial Optics today to get the ball rolling.

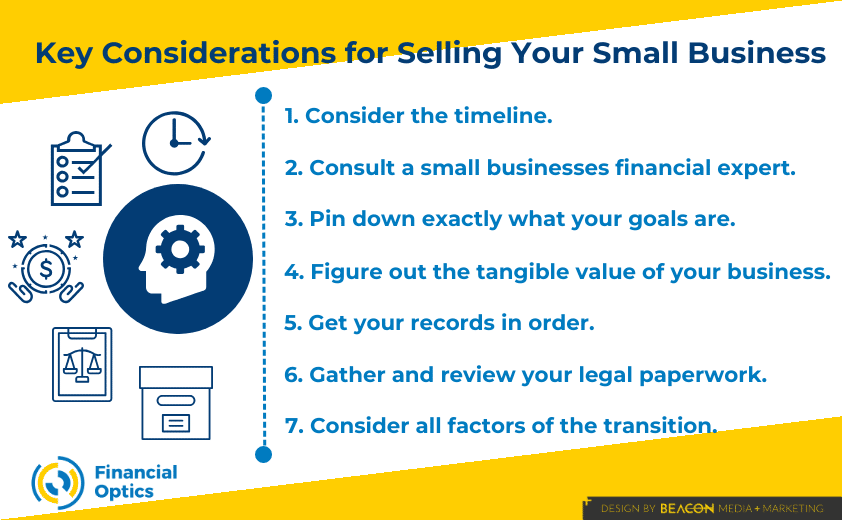

Consider the Timeline

The first thing you need to think about before selling your small business is the timeline. Often, business owners who have never sold a company before don’t realize how long the process takes. Even people who have gone through a sale in years past may need more current financial advice for small business owners due to changes in laws or the market.

So, how far ahead should you begin preparing for your sale? If you are already seriously interested in selling your small business at some point, the sooner you get ready, the better. You need to know that the sale transaction itself could take over a year. Since you need to prepare before you start that process, it is best if you begin significantly ahead of your desired sale date.

Financial Advice for Small Business Owners Is Essential Before Selling

In the months or even years before selling your small business, it pays to seek help from a financial advisor. Look for a financial services company that offers financial advice for small business owners. Even better, choose an advisory company with other services, such as small business bookkeeping and small business accounting. Then, you have a coordinated team that can support you before and during the sale.

How can a financial advisor help you with preparations? They can help you understand the tax ramifications of the sale and plan how to deal with them. With the right strategy in place, you can work towards minimizing your tax burden while maximizing your profit on the sale. A part of this plan could be weighing your options for structuring the deal in the most advantageous way to your tax situation.

In addition to your financial advisor, you should build an advisory team consisting of all the professionals you will need to guide you through selling your small business. It’s always best to have attorneys and accountants with experience in mergers and acquisitions. Begin the interviews as soon as possible and choose a team you can trust. You might want to add a business broker or an investment banker in some cases. If you are unsure about what other professionals you will need, talk it over with your financial advisor before proceeding.

Pin Down Exactly What You Want

Have you thought about what you will say when you first contact your financial advisor about selling your small business? Of course, they will need to know right away before you start the process of selling your company. That’s a given.

However, it’s hard to get a satisfying result if you only have a vague idea of what you want to achieve in the sale. Therefore, it’s best to spend some time thinking about your specific goals. What is the reason behind your desire to sell? For instance, are you looking to retire in the coming years? Do you plan to switch to a different type of business? Do you want to scale back the time you spend working? Or do you have a completely different reason?

Knowing precisely what you hope to gain allows your financial advisor to tailor their services to your unique situation and goals. Later, the buyer will also want to know why you are selling your small business. After all, why would you leave if your company is doing great? Indeed, there could be many logical reasons to sell even an outstanding company. Just remember that you need to be prepared to present them to the buyer in a positive light. Your advisory team will help you do that once they know your aims.

Know What You Have

Very early in the preparation process, you will need to address the subject of what your company is worth. Start by getting a business valuation from an objective source, such as a business accounting services company, business broker, or investment banker.

The valuation gives you helpful information about the value of your small business. When you receive the results, you will know more about the following factors of the sale:

- The market position of your business

- Your company’s financial situation

- Your business’s strengths and selling points

- Company weaknesses that you can improve before you begin the sale process

- The value of your company’s tangible and intangible assets

The business valuation is critical to a smooth and successful sale for several reasons. It helps you set realistic expectations before you begin the sale. That’s a good thing because it helps you with initial pricing and, later, with price negotiations. Knowing what your company is worth could help you spot an inadequate offer or prevent you from missing out on the best offer. Besides that, it will give you evidence of your company’s worth that you can pass on to the buyer if you choose.

Along with the current valuation, the buyer will want evidence that your company has a record of being profitable. They will want to know whether you have positioned your company to be profitable in the years ahead. A virtual CFO and small business accounting services can help you even before considering a sale. When you are ready to prepare, they can help analyze your past profits and estimate your future profitability and growth potential. With this information about your unique business, they can give you customized financial advice for small business owners in your position.

Get Your Records in Order

When you are ready to go forward with selling your small business, you will need at least three years’ worth of clean, accurate financial records. Having those records on hand and ready to go can present a challenge for many companies.

For example, many new business owners start their company with such a rush of inspiration and passion for what they do that they fail to give enough attention to setting up their small business accounting. They may even ask a relative to take care of the small business bookkeeping rather than hiring experts. Some rely on bookkeeping software but don’t think to ask for assistance, such as QuickBooks help. In other cases, a company begins on the right path, but its accountants become sloppier over time. Even if you have always ensured that your records were in order, you will need to check that they are in understandable forms.

What to Do About Your Records

Fortunately, there is a solution to the issue of having adequate records. Begin by evaluating your records to see if they are accurate and presentable. You can get help with this from your advisory team. Outsourced accounting services providers have the expertise needed to determine if your records are ready for the buyer to view.

If you are beginning your preparations at least three years before you plan to sell, the best thing you can do is start making sure your records are correctly completed. Also, consider starting the practice of requesting formal statements prepared by a small business accounting firm rather than your internal staff. These statements will then appear more objective and authoritative.

The good news is that your outsourced accounting services team can give financial advice for small business owners on what to do about have any missing, incomplete, or inaccurate records. They can help you put together the documents you need to get an accurate valuation and offer the buyer a clear picture of your company’s financial position and past profits.

Gather and Review Your Legal Paperwork

When the sale transaction eventually happens, you will be required to have all the legal paperwork from your business ready. Besides that, this paperwork may determine many aspects of the sale, including price, terms, and conditions.

Examples of legal paperwork you might need include:

- Incorporation papers

- Licensing agreements

- Permits

- Leases

- Contracts with customers and vendors

After finding these documents, review them carefully to refresh your memory about these crucial details. Then, organize them and keep them handy before and during the transaction.

Consider the Transition

Although many business owners begin with the idea that they will sell their business and make a clean exit immediately, you may want to consider leaving more gradually. Marketing your small business may be easier if you agree to help run the business for a short time.

For instance, if your unique experience and knowledge are critical to your company’s success, it might be a good idea to offer to stay on long enough to prepare the new management for success. Another option is to suggest you be involved with helping them find the right manager to take your place. Succession plans usually follow specific rules and schedules. Thus, getting financial advice for small business owners before this transition can ensure everyone is positioned for success.

Find Small Business Accounting and Financial Services at Financial Optics

If you see the day when you will sell your business approaching, don’t hesitate to seek the best small business accounting team for your company. With Financial Optics, you can get help from outsourced bookkeepers, outsourced accounting services, on-demand financial advising, and even a virtual CFO. After 30 years in the financial industry, Tim Sernett has vast knowledge and expertise to help you get ready to get the most satisfying outcome when your business sells.

Are you wondering how the proper preparation now will bring better results when you sell your small business? Contact Financial Optics to get the answers you need.